Are you prepared to make one of the most significant financial decisions of your life? Understanding the nuances of fixed-rate and adjustable-rate mortgages is crucial to navigating the homebuying process effectively.

What You Will Learn

- Fixed-rate mortgages offer consistent monthly payments, making them ideal for long-term financial planning.

- Adjustable-rate mortgages (ARMs) typically come with lower initial rates but can fluctuate over time, introducing potential risks.

- Interest rates play a crucial role: fixed rates provide stability while ARMs may save you money initially.

- Utilizing mortgage calculators can provide personalized insights into your financial situation, helping simplify the decision-making process.

- Understanding tax implications and the effect of your credit score is vital for securing favorable loan terms.

- Be aware of closing costs, which typically range from 2% to 5% of the loan amount, and review loan estimates carefully to avoid surprises.

Fixed-Rate vs. Adjustable-Rate Mortgages Comparison

Understanding the key differences between fixed-rate and adjustable-rate mortgages is crucial for making an informed decision. Below is a comparison of their core features and implications.

Fixed-Rate Mortgage

Interest Rate: Stays constant

Monthly Payments: Predictable & stable

Protection: Against rising rates

Long-Term: Ideal for stability

Benefit: Long-term financial predictability.

Adjustable-Rate Mortgage (ARM)

Interest Rate: Changes after initial period

Monthly Payments: Varies, potentially lower initially

Protection: Risk of rising rates

Long-Term: Less predictability

Benefit: Lower initial interest rates.

Key Considerations

- Tax Implications (deductible interest)

- Credit Score Effects (lower rates for higher scores)

- Closing Costs (2-5% of loan amount)

- Loan Estimates (review carefully)

Crucial for overall financial health.

Utilize Mortgage Calculators

- Monthly Payment (PITI)

- Affordability (income/expenses)

- Amortization (loan balance over time)

Personalized insights for informed decisions.

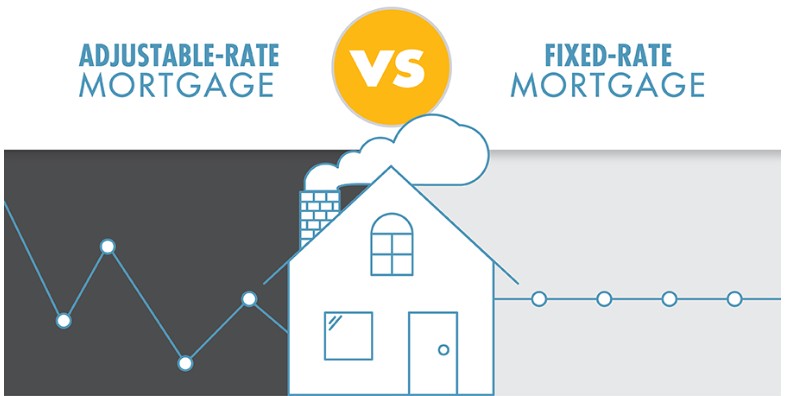

Understanding Fixed-Rate and Adjustable-Rate Mortgages

When exploring mortgage options, it’s essential to understand the differences between fixed-rate and adjustable-rate mortgages. Each has its own unique features and benefits that can fit various financial situations. As we dive deeper into these mortgage types, I’ll help you grasp their merits and how they might align with your homeownership goals! Many first-time homebuyers often feel overwhelmed by the myriad of mortgage choices available. However, gaining clarity on fixed-rate and adjustable-rate mortgages can empower you to make the best decision for your financial future.

Defining Fixed-Rate Mortgages: Key Features and Benefits

A fixed-rate mortgage offers consistency with your monthly payments, as the interest rate remains the same throughout the life of the loan. This stability is particularly appealing for those who like to plan their finances without worrying about fluctuating rates. The main features of fixed-rate mortgages include:

- Consistent monthly payments

- Long-term financial predictability

- Protection against rising interest rates

With these benefits, fixed-rate mortgages are often preferred by buyers looking for long-term homeownership. You can feel confident that your budget isn’t subject to sudden changes, allowing you to focus on other important aspects of home life!

What Are Adjustable-Rate Mortgages? Structure and Variability Explained

Adjustable-rate mortgages (ARMs) offer a different approach, where initial rates are lower than fixed-rate mortgages but can change over time. Typically, ARMs have a fixed interest rate for a specified period, after which the rate adjusts based on market conditions. Key characteristics of ARMs include:

- Lower initial interest rates

- Periodic rate adjustments

- Potential for lower payments in the early years

Understanding how ARMs function is crucial for potential homeowners. They can be quite beneficial for those planning to sell or refinance before the rate adjusts. However, they do come with some risks, which we’ll explore further in later sections.

The Role of Interest Rates in Mortgage Choices: Fixed vs. Adjustable

Interest rates are a driving force behind your mortgage decision. With a fixed-rate mortgage, you lock in a rate, providing security. In contrast, ARMs can start with lower rates but have the potential for increases, affecting your payments later on. Here’s how to think about interest rates:

- Fixed rates protect you from economic fluctuations.

- Adjustable rates can offer savings initially but may increase over time.

- Market conditions play a crucial role in both options.

By understanding these factors, you can navigate the mortgage landscape more smoothly. Making an informed decision about which type of mortgage fits your situation can make all the difference in your financial health!

Pro Tip

Did you know? Leveraging pre-approval can significantly enhance your homebuying experience. By getting pre-approved for a mortgage, you not only understand your budget better but also demonstrate to sellers that you are a serious buyer. This can give you an edge in competitive markets!

Your Path to Informed Mortgage Decisions

Making informed mortgage decisions is crucial to your financial health. With so many variables at play, it can be overwhelming. That’s why I recommend utilizing mortgage calculators and other interactive tools to help guide you through the complexities of mortgage options. These tools can provide personalized insights based on your financial situation, helping you understand what monthly payments might look like and how different mortgage types could affect your long-term finances!

Utilizing Mortgage Calculators and Interactive Tools for Personalized Insights

Mortgage calculators are invaluable resources that simplify the decision-making process. They allow you to input various factors, such as loan amount, interest rate, and loan term, to see potential outcomes. Here are some calculators that I find particularly useful:

- Monthly Payment Calculator: Helps estimate your monthly payment based on principal, interest, taxes, and insurance.

- Affordability Calculator: Determines what you can comfortably afford based on your income and expenses.

- Amortization Calculator: Illustrates how your loan balance decreases over time and how interest is applied.

By leveraging these tools, you can gain a clear understanding of your mortgage options and feel more confident in your decisions!

Key Considerations: Tax Implications and Credit Score Effects of Mortgages

As you consider your mortgage options, it’s essential to think about the broader financial implications, such as tax deductions and how your credit score influences your loan terms. Mortgage interest can often be tax-deductible, which may lower your overall tax burden. Your credit score, on the other hand, plays a crucial role in determining the interest rates available to you. Higher scores typically lead to lower rates, which can save you significant money over the life of the loan. If your score isn’t where you’d like it to be, there are steps you can take to improve it before applying!

Understanding Closing Costs and Loan Estimates in Mortgage Applications

Another vital consideration is understanding closing costs and reviewing your loan estimates carefully. Closing costs can include various fees, such as appraisal fees, title insurance, and lender charges. It’s essential to budget for these costs, as they typically range between 2% to 5% of the loan amount. When you receive a loan estimate, ensure you read through it thoroughly. This document outlines your loan terms, estimated monthly payments, and closing costs. If anything seems unclear, don’t hesitate to reach out for clarification! Being well-informed helps you avoid surprises later on.

Frequently Asked Questions (FAQs)

- What is the main difference between a fixed-rate and an adjustable-rate mortgage?

- A fixed-rate mortgage maintains the same interest rate and monthly payments throughout the loan’s life, offering stability. An adjustable-rate mortgage (ARM) starts with a lower interest rate that can change after an initial period, leading to variable monthly payments.

- What are the benefits of a fixed-rate mortgage?

- Fixed-rate mortgages offer consistent monthly payments, long-term financial predictability, and protection against rising interest rates, making budgeting easier and providing peace of mind.

- When might an adjustable-rate mortgage (ARM) be a good option?

- An ARM might be beneficial for individuals who plan to sell or refinance their home before the initial fixed-rate period ends, or for those who anticipate a significant increase in their income that will offset potential rate increases.

- How does my credit score affect my mortgage options?

- Your credit score significantly influences the interest rates you qualify for. A higher credit score typically leads to lower interest rates on both fixed-rate and adjustable-rate mortgages, resulting in substantial savings over the loan term.

- What are closing costs, and how much should I expect to pay?

- Closing costs are various fees associated with finalizing your mortgage, such as appraisal fees, title insurance, and lender charges. They typically range from 2% to 5% of the total loan amount and must be paid at the time of closing.

Recap of Key Points

Here is a quick recap of the important points discussed in the article:

- Fixed-rate mortgages provide consistent monthly payments and long-term financial predictability.

- Adjustable-rate mortgages (ARMs) offer lower initial rates but can adjust based on market conditions.

- Interest rates play a crucial role in mortgage decisions; fixed rates protect against fluctuations while ARMs may offer initial savings.

- Utilizing mortgage calculators can help you understand potential payments and financial impacts effectively.

- Consider tax implications and your credit score as they significantly affect loan terms and overall costs.

- Understand closing costs and review loan estimates thoroughly to avoid surprises.