Calculating mortgage payments is essential for budgeting and understanding your loan costs. For a fixed-rate mortgage, the monthly payment covers principal and interest, based on a standard amortization formula. This guide walks you through the process step-by-step, including the math behind it.consumerfinance.govrocketmortgage.com

The Mortgage Payment Formula

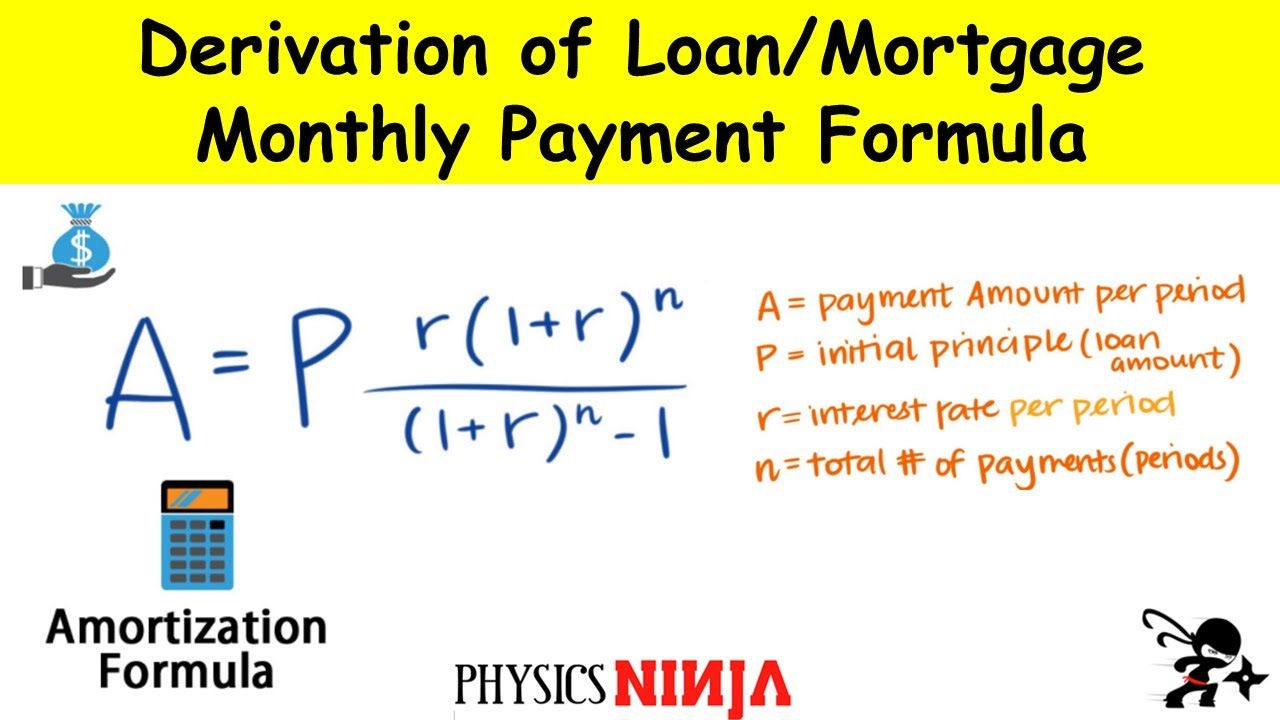

The formula for the monthly principal and interest payment (M) on a fixed-rate mortgage is derived from the concept of an amortizing loan, where payments are constant but the split between interest and principal changes over time. Here’s the formula:

M=Pr(1+r)n(1+r)n−1 M = P \frac{r(1 + r)^n}{(1 + r)^n – 1} M=P(1+r)n−1r(1+r)n

Where:

- P is the principal loan amount (the total amount borrowed).

- r is the monthly interest rate (annual interest rate divided by 12, in decimal form).

- n is the total number of payments (loan term in years multiplied by 12).

This equation comes from solving for the present value of an annuity, ensuring the sum of all payments repays the loan plus interest.bankrate.comen.wikipedia.org

Derivation of Loan/Mortgage Monthly Payment Formula

Step-by-Step Guide to Calculate

To arrive at the monthly payment, follow these structured steps:

- Gather Your Loan Details: You’ll need the principal (P), annual interest rate (as a percentage), and loan term in years. For example, P = $200,000, annual rate = 4%, term = 30 years.

- Convert Annual Rate to Monthly Rate (r): Divide the annual rate by 12 and convert to decimal. For 4%: r = 4 / 12 / 100 = 0.003333…

- Calculate Total Number of Payments (n): Multiply years by 12. For 30 years: n = 30 * 12 = 360.

- Compute the Power Term: Calculate (1 + r)^n. Using the example: (1 + 0.003333)^360 ≈ 3.3102.

- Apply the Formula:

- Numerator: r * (1 + r)^n = 0.003333 * 3.3102 ≈ 0.011034

- Denominator: (1 + r)^n – 1 ≈ 3.3102 – 1 = 2.3102

- Multiplier: Numerator / Denominator ≈ 0.011034 / 2.3102 ≈ 0.004777

- M = P * Multiplier = 200,000 * 0.004777 ≈ $954.83

This step-by-step breakdown ensures transparency: start with inputs, perform conversions, compute intermediates, and arrive at the final payment.rocketmortgage.comidfpr.illinois.gov

Example Calculation

Using the details above ($200,000 loan at 4% over 30 years), the monthly payment is approximately $954.83. Over the loan’s life, you’d pay about $143,739 in interest, totaling $343,739.

For visualization, here’s a graph showing how equity builds and debt decreases over time:

Mortgage Formula (with Graph and Calculator Link)

Additional Considerations

- Taxes, Insurance, and PMI: The full monthly payment (PITI) includes property taxes, homeowners insurance, and possibly private mortgage insurance (PMI) if your down payment is less than 20%. Add these to the principal and interest amount.

- Tools for Ease: While manual calculation builds understanding, use online calculators for quick results or to include extras like taxes.

- Variable Rates: For adjustable-rate mortgages (ARMs), payments can change; the formula applies to the initial fixed period.

By mastering this formula, you can compare loan options or estimate affordability accurately.